2 / 22

2 / 22

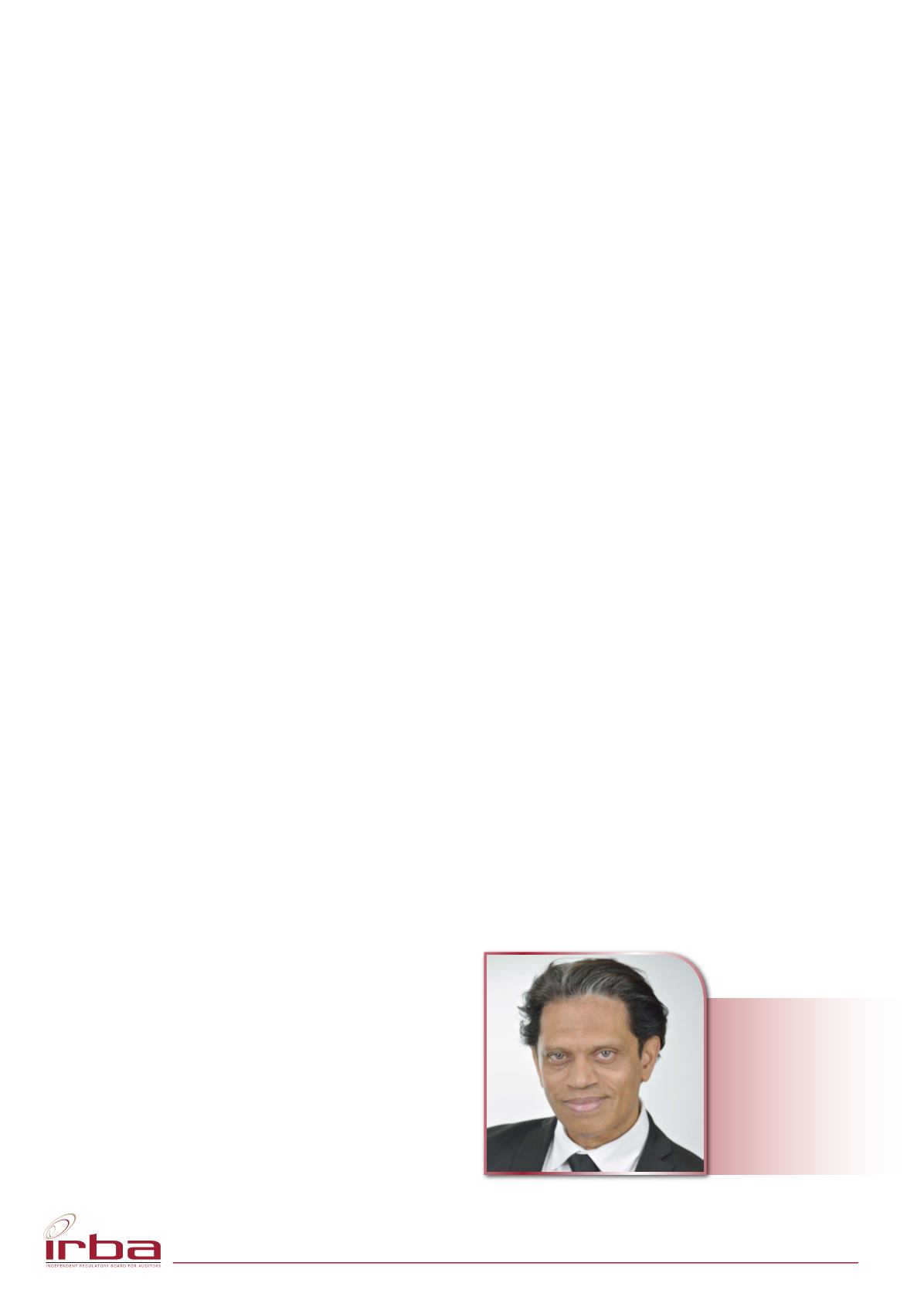

FROM THE CEO’S DESK

Bernard Peter Agulhas

Chief Executive Officer

The past 18 months have been tumultuous, and 2018 will go down

in audit history as one when the profession hit a crossroad. Through

this time, our general advice to audit firms has been to take actions

that will restore confidence as that cannot be done by the regulators

alone. Firms have a key role to play in rebuilding trust in their quality

and integrity. We have also emphasised that all role players in the

financial reporting system, including management, those charged

with governance, internal auditors and shareholders, have a role to

play in restoring confidence in the profession.

The Steinhoff business failure cost the economy billions of rand. In

the latest scandal with VBS Bank the auditor provided a clean audit

report though millions of rand had been stolen and pensioners had

lost their hard-earned investments.

Audit is a public interest responsibility. As such, auditors must

consider the cost of their decisions on the public, investors and the

economy.

During our engagement with the profession this year it became clear

that the firms also do not see the gravity of reputational damage,

and they do not realise the extent of the measures that need to

be taken to reverse this. During past crises when there had been

a loss of confidence, the first reaction had always been to deny

that anything is wrong. Rather, there had always been an insistence

that audit quality meets the required standard, while regulators have

seen things differently, with inspection results supporting our view.

Auditors do not only require technical competence to perform a

high-quality audit – they also require appropriate behavioural

competence, and this is something that I have repeatedly addressed

this year. Most audit failures are not only linked to poor audit quality.

They have a lot to do with auditors behaving unethically, not

exercising professional scepticism and not acting independently.

Furthermore, if leadership supports a culture that makes profits

more important than ethical behaviour, this tone will permeate the

whole organisation. Initially, we thought that the unethical behaviour

was isolated, but as more wrongdoings have come to light, it is

becoming clearer that we are dealing with a systemic problem in

the profession.

It takes one “bad apple” for a firm, and indeed a profession, to

be classified as a “barrel of rotten apples”. Therefore, individual

errant partners should be dealt with swiftly as drawn out processes

of disciplining auditors benefit no one and merely perpetuate the

negative image of the profession. The IRBA is making every effort

to get these processes concluded as quickly as possible in order

to minimise the reputational damage to the profession as a whole.

I wish to emphasise that the regulator is there to assist the firms

and caution them against potential audit failures. It is, therefore,

advisable to work with us instead of opposing our attempts to help

improve audit quality.

Times have also changed with regards to the environment in which

we find ourselves. There is an increased awareness of the role of

auditors and expectations by investors, the media and the public.

The “new normal” is an active media as well as an educated and

vocal public. The advent of social media has changed the speed at

which the public forms its conclusions.

It seems that auditors have forgotten who the ultimate client is, and

whose expectations they must satisfy. Being too cosy with the client

can mean that the auditor is no longer comfortable to challenge the

client on behalf of shareholders and investors. The expectation gap

is therefore real.

The public expects more work to be done by auditors around

fraud risks. Consequently, firms must improve and adapt their

methodologies and work done around fraud risk on the engagement.

It is no longer sufficient to claim that auditors are not expected to

discover fraud. Rather, auditors need to strengthen their procedures

so as to identify and respond to fraud risk factors, especially in the

current environment of corruption and increased expectations from

the public.

Much of what has happened has confirmed the concerns we

voiced as far back as 2013 and 2014. We see that there is a lack

of professional scepticism and independence, and conflicts of

interest are not considered sufficiently. Many audit failures are a

result of cosy relationships between auditors and their clients (audit

committees, CFOs, management). Yet, auditors keep denying that

these relationships have an impact on their independence and audit

opinions.

It is time for auditors to start to take responsibility and accountability

and stop being in denial and defensive. In 2019, there must be a

commitment to clean up and focus on audit quality, especially in light

of the IFIAR Public Report on audit findings and the deterioration in

quality. Similarly, the IRBA will address any potential shortcomings in

its regulatory oversight in its attempts to rebuild public confidence.

My hope for this holiday season is that we will all reflect on the year

that was and resolve to make significant changes in 2019. I hope

firms seriously start focusing on quality, not as a risk to be managed

but as an imperative to regain public trust. Without trust there is no

confidence; and without confidence an audit opinion has limited

value.

Let’s not wait for the market to change audit and decide on

its continued relevance. Let’s agree to make the changes in the

profession that are necessary to ensure that the profession can

weather this storm.

I wish you all a good festive season and a wonderful holiday break.

My hope for 2019 is that we can finally draw a line in the sand and

move forward with renewed hope for the profession.

Issue 44 | October-December 2018

2