11 / 18

11 / 18

EDUCATION AND TRANSFORMATION

THE IRBA’S TRANSFORMATION WORKSHOPS

For the IRBA, bringing positive change into the profession is of

major importance – and one of those critical changes is having a

profession that embraces and acts on the tenets of transformation.

Ensuring that this is realised, though, means the regulator has to rely

on collaborations with other stakeholders, such as the audit firms,

the Auditor-General South Africa and the South African Institute of

Chartered Accountants (SAICA).

These collaborations, however, have been but one plan that the IRBA

has been involved in in its drive to see the profession transformed.

The regulator took the initiative to develop a strategy that addresses

areas where it could influence the advancement of transformation

in the profession. This has culminated into a Transformation Project

List that is updated annually.

As part of this project list, the IRBA commissioned an independent

research study to explore factors driving and limiting professional

advancement in auditing. To share and discuss the results of this

research study, as well as establish common ground and solutions

for a way forward, the IRBA conducted workshops with key

stakeholders. Workshops were held in Johannesburg, Cape Town,

Durban and Pretoria.

The workshops also afforded the attendees an opportunity to share

their experiences and/or programmes implemented to promote and

respond to transformation challenges.

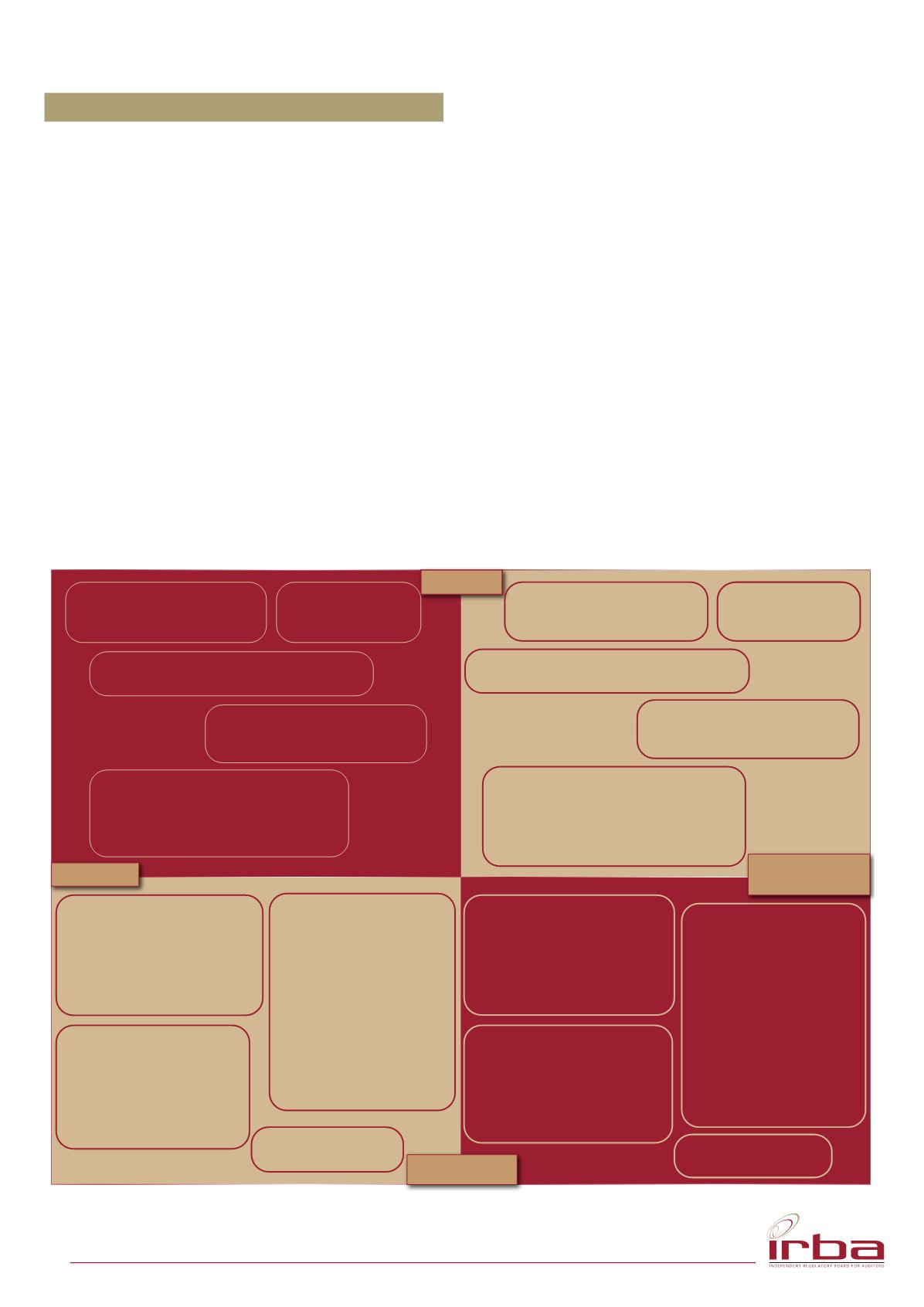

Background to the IRBA’s Transformation Study

The Diversity and Transformation Study conducted by an

independent research company, Answered Insight, sampled

two groups during 2015. One sample was the IRBA database of

accounting students who were completing articles at an accounting

or auditing firm. The second sample was drawn from the SAICA

database of registered CAs.

The comprehensive research covered perceptions of work,

education, training, career, work experiences, auditing as a career,

the difference between a CA and an RA, as well as the attractiveness

of auditing as a career, among other issues. Most respondents

were from auditing or accounting firms, with others coming from

a diverse range of listed companies, state-owned enterprises,

financial sector organisations and private sector companies from

an array of industries.

The image below gives a high-level overview of the results of the

survey.

Why accounting?

• Career opportunities 60%

• Financial security 49%

Why accounting?

• Career opportunities 62%

• Financial security 53%

During studies

• Appeal of moving from home town 42%

During studies

• Appeal of moving from home town 40%

During articles

• Diverse range of work 88%

• Good work environment 83%

During articles

• Good work environment 89%

• Diverse range of work 85%

RA (of those would consider)

• Respect 95%

• Open other opportunities 93%

• Increase marketability 90%

• Financial 84%

RA (of those would consider)

• Respect 85%

• Open other opportunities 85%

• Financial 83%

• Like responsibility 78%

• Increase marketable 78%

RA (of those would

not consider)

• Late nights/stress 82%

• Auditing as a profession

82%

• Additional training

period 65%

RA (of those who would

not consider)

• Auditing as a profession

85%

• Late nights/stress 78%

• Do not enjoy auditing

74%

39% expect extra

exam to become RA

20% expect extra

exam to become RA

During articles

• Salary dissatisfaction

73%

• Killed auditing

passion 44%

• Unfair job assignment

39%

• Unfair performance

appraisals 46%

• Stress and pressure

overwhelming 51%

• Lack of support

during articles 26%

During articles

• Salary dissatisfaction

66%

• Unfair performance

appraisal 44%

• Stress and pressure

overwhelming 51%

• Killed auditing

passion 42%

• Unfair job assignment

38%

• Lack of support

during articles 19%

Main influencers

• Parents 39%

• Teachers 26%

Main influencers

• Parents 43%

• Teachers 28%

During studies

• 3 year difficulties 65%

• 2 year difficulties 34%

• Coping with school to

university transition 51%

• Difficulty balancing study

and personal life 41%

rd

rd

During studies

• 3 year difficulties 54%

• Coping with school to

university transition 35%

• Difficulty balancing study

and personal life 34%

• 2 year difficulties 29%

rd

nd

DRIVERS

QUALIFIED

PROFESIONALS

TRAINEES

DETRACTORS

Issue 43 | July-September 2018

11