16 / 22

16 / 22

Issue 35 | July-September 2016

16

auditors on 5 September 2016, providing guidance on the process

to be followed for all SVDP-related RIs identified. We encourage

all of our registered auditors to familiarise themselves with the

contents of this communique, a copy of which can be found on

our website

(http://www.irba.co.za/news-events/communiques)under the heading “Legal”.

Holding Outs

On 9 September 2016 Michaelangelo Andile Jordan pleaded

guilty to, and was found guilty of, contravening Section 41 of the

Auditing Profession Act No. 26 of 2006 in the Durban Specialised

Commercial Crime Court. The accused was cautioned and

discharged.

Practice Related Matters

Occasionally, practice related matters find their way to the Legal

Department. We share the body of our response to an enquiry

that has arisen in this way, for your information and guidance. The

situation concerned a sole practitioner who had been hospitalised.

The enquiry came from a practitioner who was offering to “care-

take” the practice.

We urge all practitioners, particularly sole practitioners, to consider

this scenario in their own practices, and ideally to commence

succession planning sooner rather than later.

“I draw your attention to paragraph 150.5 of the Code of

Conduct, which reads as follows:

‘A registered auditor shall not delegate to any person who is

not a partner, or fellow director, the power to sign audit, review

or other assurance reports or certificates that are required, in

terms of any law or regulation, to be signed by the registered

auditor responsible for the engagement. In specific cases where

emergencies of sufficient gravity arise, however, this prohibition

may be relaxed, provided the full circumstances giving rise to

the need for delegation are reported both to the client of the

registered auditor concerned and to the Regulatory Board.’

It appears to me that the situation you outline would fall within

the “emergencies of sufficient gravity” proviso of this paragraph.

I assume that the family member with the Power of Attorney

would be able to make the delegation, on behalf of the critically

ill and incoherent RA.

You would then be able to accept this delegation provided the

circumstances are reported to both the Regulatory Board (and I

am prepared to accept your email of 21 July 2016 as this report)

and to the clients concerned.

TheCodeapplies toa specificsituation. Should thecircumstances

change, and should your responsibilities change such that you

become the engagement partner on any engagement, this

provision in the Code will not apply, and you will have to assume

full responsibilities in terms of the ISAs and the IRBA Code for

the engagement.

It would probably be prudent to inform both your and the other

RA’s insurers.

I would accordingly await your confirmation that the clients have

been informed of this situation.

I must also inform you that any such delegation will be

communicated to the Inspections Department so that they are

aware of the circumstances, and can act appropriately should

the firm in question be selected for inspection. It follows that you

would need to inform us of the name of the practitioner.

I trust that this answers your query and I await your further

communication in due course.”

In addition, SAICA has published an article, which remains relevant,

in ASA of October 2014, which can be accessed on the SAICA

website.

Subsequent to this matter being drawn to our attention, we

received a call from a most distressed trainee accountant, from a

different firm, informing us that the sole proprietor of the firm had

passed away – unexpectedly – that morning, and asking what to

do.

I hope that sole practitioners will take heed of these scenarios and

ensure that they do not land in a similar situation. The situation is

exacerbated when the practice is the major asset in the deceased

estate, and there is a widow to support. Clients who are not in a

position to wait for legal formalities to take place will leave to find

new auditors, and the value of the practice, and the ability to sell it

as a going concern, will diminish rapidly.

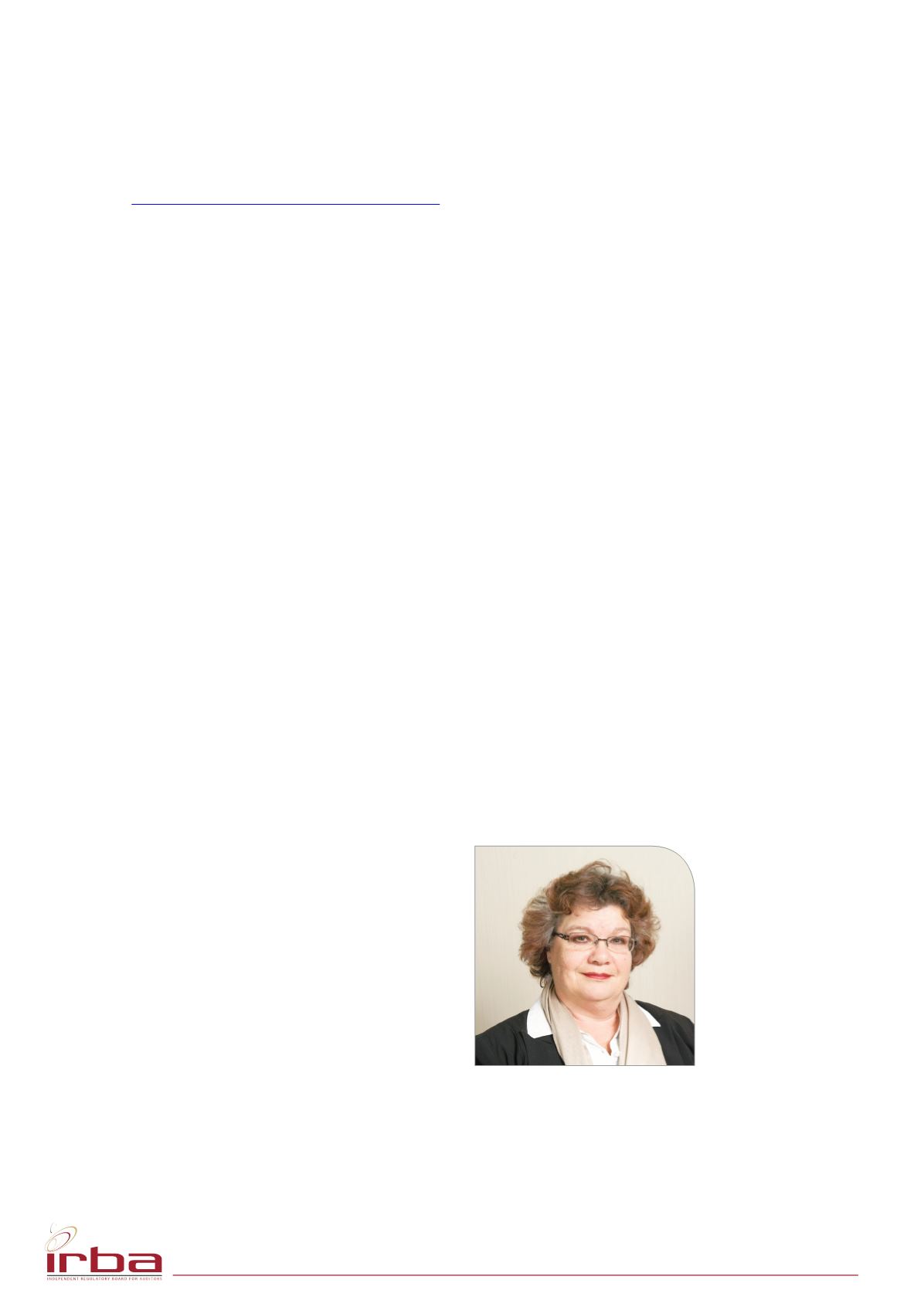

Jane O’Connor

Director Legal

Telephone: (087) 940-8804

Fax: (087) 940-8873

E-mail:

legal@irba.co.zaLEGAL

c o n t .